/cloudfront-us-east-2.images.arcpublishing.com/reuters/H6M3G5CBSBIETPXWCWSGL3ZZAE.jpg "Analysis: A court battle raises the question – how far will Japan swallow poison pills?")

Business office buildings are pictured at a company district in Tokyo, Japan, February 12, 2017. Photo taken February 12, 2017. REUTERS/Toru Hanai

TOKYO, Oct 21 (Reuters) – The destiny of long term hostile takeover bids in Japan could rest on an impending courtroom ruling that will determine whether or not the country’s top maker of newspaper printing presses can go ahead with a poison tablet towards an unwelcome shareholder.

At situation is irrespective of whether 105-12 months-aged Tokyo Kikai Seisakusho Ltd (6335.T) will be allowed to not count votes from Asia Growth Money (ADC) (9318.T) – an expenditure agency that built up most of its 40{e421c4d081ed1e1efd2d9b9e397159b409f6f1af1639f2363bfecd2822ec732a} stake in a issue of weeks – when shareholders vote on issuing new stock that would dilute ADC’s ownership.

A holding of more than 33{e421c4d081ed1e1efd2d9b9e397159b409f6f1af1639f2363bfecd2822ec732a} in Japan gives the stakeholder veto rights above important board conclusions and often de facto control.

ADC has sought an injunction and the Tokyo District Court’s ruling – the to start with one particular to look at an try to exclude an investor from a shareholder vote on a poison pill – is anticipated sometime in the next 7 days. A victory for Tokyo Kikai retains the opportunity to make it much less difficult for other Japanese businesses to use poison pills.

Tokyo Kikai, which has claimed ADC hurts its company worth, will set the poison capsule program to a shareholder vote at an incredible standard conference on Friday.

The struggle highlights equally a increase in hostile takeovers in Japan more than the past number of a long time as the exercise – once thought of the area of unscrupulous corporate raiders – loses its stigma as perfectly as what some specialists see as inadequate Japanese takeover procedures that depart providers, compact kinds specially, much too defenceless.

It also arrives at a time when traders are observing to see if a travel by Japan’s new key minister, Fumio Kishida, to roll back again some of the professional-market guidelines of previous premier Shinzo Abe will influence company governance.

Corporate governance industry experts say it is as well hard to contact which way the court may rule.

On just one hand, ADC’s argument that a ruling in Tokyo Kikai’s favour would fly in the face of shareholder equality is a strong a person as the basic principle is enshrined in Japanese company regulation, they say.

“If a goal organization can find who is permitted to vote on a poison tablet, it will occur up with all forms of excuses to develop a checklist of qualified shareholders who have the very best probability of passing the capsule,” reported Takumi Watanabe, government officer at proxy advisory company QuestHub.

But governance professionals incorporate the court docket could possibly come to a decision that ADC counts as an “abusive buyer” that could threaten the rights of minority shareholders, possessing speedily crafted up its stake and not introduced the corporation or other shareholders with a new management program.

IT Wouldn’t Come about Abroad

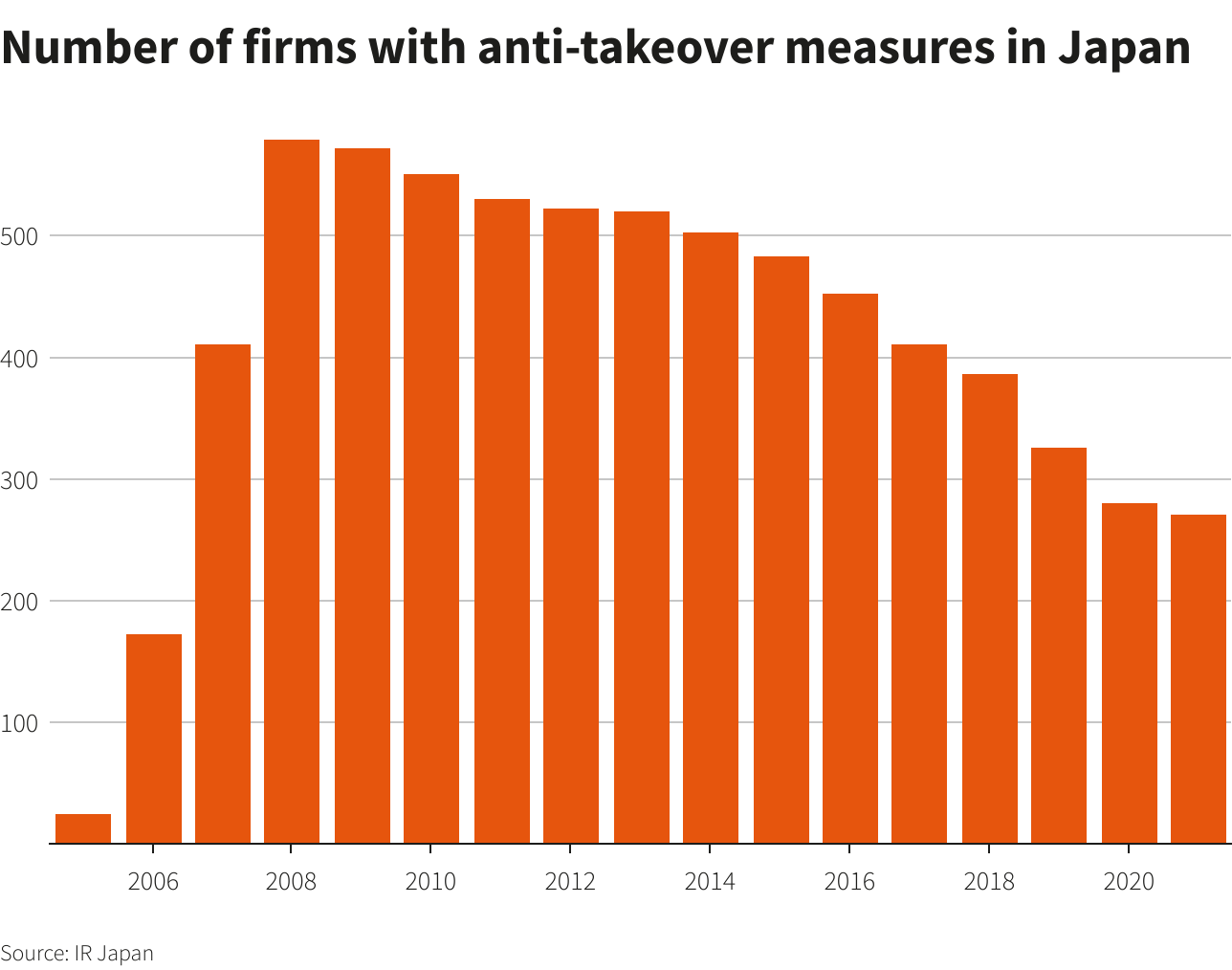

Approximately a decade in the past, much more than 500 Japanese corporations had a permanent poison pill, commonly part of their company’s content articles of incorporation. But the practice – oft criticised for entrenching negative administration – fell out of favour soon after corporate governance reforms pushed by Abe necessary institutional traders to disclose how they voted on agenda objects at shareholder meetings, which includes poison products.

A poison pill that targets a certain bidder – termed an unexpected emergency poison capsule in Japan – was very first correctly utilized very last yr by Toshiba Device, renamed Shibaura Device (6104.T), in its battle towards notable activist investor Yoshiaki Murakami.

Because then at minimum five other companies such as Tokyo Kikai have possibly introduced them or sought to introduce them. Amid them, Shinsei Financial institution (8303.T)options to seek out shareholder approval for a poison capsule to thwart on the internet economic conglomerate SBI Holdings’ (8473.T) $1.1 billion bid.

Authorities say the recent wave of poison capsule exercise underscores a absence of clarity above what Japanese companies can do to block takeover bids.

“Appropriate now, officers at providers are scratching their heads more than what’s permitted or not,” explained Atsuko Furuta, director at trader relations consulting firm IR Japan.

They be aware Japanese modest cap corporations are particularly vulnerable to aggressive stake-setting up from unwelcome stakeholders. Tokyo Kikai, for instance, has a industry price of just 15 billion yen ($130 million).

Not like the United States, Japanese organization boards simply cannot quickly adopt a poison capsule to ward off a hostile suitor. Though not explicitly composed in regulation, court docket precedents have led them to believe that they ought to seek out shareholder approval ahead of adopting a poison tablet – a time-consuming system.

In Europe, tender offers are normally mandatory for acquisitions of stakes further than a sure threshold – 30{e421c4d081ed1e1efd2d9b9e397159b409f6f1af1639f2363bfecd2822ec732a} in the British isles – a rule that would avoid instances like Tokyo Kikai’s.

Wataru Tanaka, a corporate law professor at the College of Tokyo, thinks the government should really prioritise correcting the country’s takeover regulations.

“Poison supplements are a 2nd-very best remedy,” he explained.

($1 = 114.3800 yen)

Reporting by Makiko Yamazaki Supplemental Reporting by Yuki Nitta Modifying by David Dolan and Edwina Gibbs

Our Benchmarks: The Thomson Reuters Have confidence in Principles.